How long before petrol, diesel prices rise in India amid global oil shock?

The West Asia war has triggered a major global crude oil supply shock, but India's petrol and diesel rates have remained unchanged since May 2022. We spoke to experts to understand how much longer India can keep fuel prices steady.

")

While fuel prices have risen across many countries, petrol and diesel rates at pumps across India have remained unchanged. (Photo: PTI)

New Delhi,UPDATED: Apr 22, 2026 21:24 IST

For more than a month, the war in West Asia has kept global oil markets on edge. Crude prices have jumped sharply, key supply routes have come under scrutiny, and energy-importing nations are already paying more for their energy imports.

Petrol and diesel prices have risen across several countries as governments and consumers absorb higher import costs. Yet at petrol pumps across India, retail fuel prices have remained unchanged, creating a rare pocket of calm in an otherwise volatile global energy market.

For consumers, that has meant relief. For India’s oil marketing companies (OMCs), it has meant carrying a growing burden.

State-run fuel retailers such as Indian Oil Corporation, Bharat Petroleum Corporation Limited and Hindustan Petroleum Corporation Limited have weathered such phases before, using refining profits, inventory gains and balance-sheet strength to cushion shocks.

But analysts say those buffers are not endless, especially if crude prices remain elevated or move higher.

HOW MUCH ARE OIL COMPANIES LOSING?

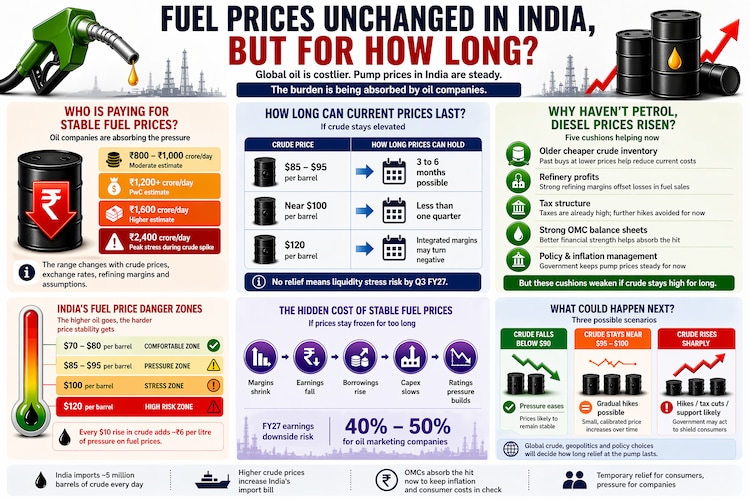

There is no single number that captures what oil companies are absorbing right now. The burden changes with crude prices, exchange rates, refining margins and domestic fuel demand.

But analysts agree on the broad trend: companies are sacrificing margins to keep pump prices steady.

Manas Majumdar, Partner and Oil & Gas Sector Leader at PwC India, told indiatoday.tech that Indian oil companies are “getting squeezed from both sides of the barrel” as global crude prices have risen while domestic retail prices remain unchanged.

He said the Indian crude basket had risen to around $110-plus per barrel at one stage, while India was sourcing additional barrels from further markets such as South America and earlier Russian crude discounts had faded, increasing procurement costs.

Majumdar estimated that with petrol prices near Rs 95 per litre in Delhi, and after accounting for taxes, oil companies may be facing losses of around Rs 15 to Rs 20 per litre on petrol and even higher on diesel, translating into daily marketing losses of over Rs 1,200 crore.

Arun Kailasan, Research Analyst at Geojit Investments Limited, said that at crude levels of around $95 per barrel, Indian oil marketing companies are “absorbing losses of roughly Rs 1,600 crore per day (Rs 48,000 crore monthly).”

He said companies are absorbing under-recoveries of around Rs 18 per litre on petrol and Rs 35 per litre on diesel, meaning they are selling fuel below what prevailing costs would normally justify. “Every US$10 per barrel rise adds around Rs 6 per litre of incremental pressure,” he told indiatoday.tech.

Kailasan added that during the most recent crude spike, estimated sector-wide losses had briefly crossed Rs 2,400 crore a day, or nearly Rs 72,000 crore a month, showing how quickly pressure can build when oil surges sharply.

A more moderate reading came from Puneet Singhania, Director at Master Capital Services Limited.

“Crude is hovering around $85 to $95 per barrel, but retail fuel prices haven’t moved, which means marketing margins on petrol and diesel are barely breaking even or slightly negative, roughly Rs 1 to Rs 3 per litre,” he said.

“We’re looking at roughly Rs 800 crore to Rs 1,000 crore per day across OMCs, which can add up to about Rs 25,000 crore to Rs 30,000 crore over a month if this continues.”

The estimates vary because assumptions vary. But whether the stress is mild or severe, the direction is the same: somebody is paying for stable fuel prices, and right now much of that cost sits with the companies.

WHY PETROL, DIESEL PRICES HAVEN'T CHANGED

Fuel prices in India do not rise every time crude oil becomes costlier. The price you pay at the pump depends on several moving parts, not just global oil rates.

Taxes charged by the Centre and states, the rupee-dollar exchange rate, transport costs, refinery profits, and older cheaper crude bought earlier all play a role in deciding the final retail price.

Manoranjan Sharma, Chief Economist at Infomerics Ratings, explained that fuel pricing is not a simple formula where crude rises today and petrol rises tomorrow. “The system operates dynamically between crude costs, refining margins, exchange rates, taxation, and retail pricing,” he said.

In simple words, oil companies have a few buffers that help them delay price hikes for some time.

For example, if companies had already bought crude earlier at lower prices, they could still benefit from that stock. If refineries are earning strong profits, some of that money can offset losses in fuel sales. If the rupee stays stable, imported crude becomes less expensive than it would otherwise be.

Sharma said this works like a temporary support system built on inventory gains, refinery earnings, company finances, policy decisions and fuel demand.

That cushion matters because India consumes roughly 5 million barrels of oil a day. At that scale, even small increases in crude prices can quickly swell into large sector-wide costs.

In the short term, oil companies can absorb some of that pressure through older lower-cost inventory, stronger refinery earnings and internal buffers. That is why petrol and diesel prices can remain unchanged for a while even when crude prices are rising globally.

But if higher oil prices persist, those cushions begin to wear thin.

WHY ELECTIONS OFTEN MATTER

Fuel prices are not just an economic issue in India. They also carry political weight because they directly affect household budgets, transport costs and inflation sentiment.

That is why any change in petrol and diesel prices tends to draw sharper public attention during election seasons, when rising everyday costs can quickly become a voter issue.

Past episodes show why timing often comes under scrutiny. In November 2021, the Centre cut excise duty on petrol and diesel ahead of key state elections, while several states later reduced VAT.

In March 2022, after assembly elections in Uttar Pradesh and four other states concluded, fuel prices were raised in a series of revisions following a long pause. In March 2024, petrol and diesel prices were cut by Rs 2 per litre ahead of the Lok Sabha election schedule.

Officially, those decisions were framed as steps to provide consumer relief, contain inflation and respond to prevailing economic conditions.

The current political calendar is also nearing an important marker. Voting in the second and final phase of the West Bengal Assembly election concludes on April 29, bringing an end to the 2026 state election cycle that also included Assam, Kerala, Tamil Nadu and Puducherry. Counting of votes across all five contests is scheduled for May 4.

That does not by itself indicate any connection with current fuel prices. Retail pricing decisions today depend on a mix of crude oil costs, company margins, taxes, exchange rates and inflation management.

Even so, past precedents mean markets and consumers often watch the political calendar alongside global oil prices when assessing whether fuel price revisions could eventually follow, especially as oil companies continue to absorb losses to keep rates stable.

WHEN COULD PETROL, DIESEL PRICES RISE?

From a technical point of view, analysts say the answer depends largely on what happens to crude oil next amid the ongoing West Asia war.

Singhania said, “As long as crude stays in the $85 to $95 range, they can probably hold prices steady for a quarter or two, though profitability will remain tight.”

That implies a window of roughly three to six months if oil remains near current levels.

But if crude moves higher and stays there, the cushion could thin quickly. “The real problem starts if crude moves higher and sustains above $100 per barrel. That’s when margins come under real stress and cash flows start tightening,” Singhania said.

Sharma offered a similar warning. “If crude approaches $100 per barrel, the sustainability window may shrink to less than a quarter,” he said.

He added that sustained losses beyond Rs 3 to Rs 4 per litre become difficult to absorb without either fuel price hikes or government support. That suggests the room to absorb losses could narrow to under three months if crude enters triple digits and remains elevated.

Kailasan added that at current run rates, “existing profit buffers are largely depleted, making the current pricing stance difficult to sustain beyond the near term without either price hikes or fiscal intervention.”

Majumdar said OMCs built healthy balance sheets over the last 1.5 to 2 years, helped by periods when crude fell near $60 per barrel while retail prices did not decline proportionately. But at current loss levels, those buffers could erode within the next three to four months without major fiscal support or retail price changes.

He added that Indian OMCs typically operate comfortably when crude remains in the $70 to $80 per barrel range. If prices fall below $90 per barrel, pressure could ease. But if crude rises towards $120 per barrel, even combined refining and marketing margins could turn negative.

Majumdar also warned that if crude stays elevated and no relief emerges through phased hikes or lower oil prices, companies could begin facing liquidity stress by Q3 FY27.

THE COST OF KEEPING FUEL PRICES LOW

Stable prices can be politically useful and consumer-friendly in the short term. Financially, however, they come with trade-offs.

The first casualty is marketing margin, the spread companies earn on selling fuel. If that turns negative, firms become more dependent on refining profits to protect earnings.

But refining is cyclical. Strong margins today do not guarantee strong margins tomorrow.

Sharma said prolonged price rigidity can trigger “rising earnings volatility, EBITDA compression, increased working capital needs, higher leverage, and declining return ratios.”

That means profits become less predictable, borrowing needs rise and balance sheets lose flexibility.

Singhania said the pressure would eventually become visible in returns and investment capacity as well. “If prices remain unchanged for a longer period, the impact on OMCs like IOC, BPCL, and HPCL will start showing more clearly. The first hit is on marketing margins, which are already under pressure and could turn negative if crude stays elevated.”

Majumdar said prolonged price disruption beyond a couple of quarters could significantly contract EBITDA, while earlier single-digit positive marketing margins have already begun eroding.

He added that FY27 earnings estimates could see a 40-50% downside if under-recoveries persist, forcing companies to cut other spending and capital expenditure.

Higher short-term borrowings to fund expensive crude cargoes may also pressure interest coverage ratios, while a prolonged regulated margin squeeze could weigh on credit ratings and future fund-raising for expansion and energy transition plans, he said.

WILL PETROL, DIESEL PRICES RISE SOON?

There is no official indication of an immediate hike in petrol or diesel prices. But historically, when cost pressures build for too long, revisions are often gradual rather than sudden.

Small increases spread over time are easier to absorb than one sharp jump.

Sharma said “sustained losses beyond Rs 3 to Rs 4 per litre become untenable without price hikes or government support.”

That leaves a familiar set of options: calibrated pump price increases, tax adjustments, or fiscal support.

But whether fuel prices could rise depends on two important things. The first is crude oil itself. If global prices cool, much of the pressure eases naturally. The second is $100 per barrel. If crude climbs there and stays there, the room to shield consumers could narrow quickly.

Fuel prices are unchanged for now. But if crude oil prices stay high for a longer period, that may become harder to sustain.

- Ends