From the Editor-in-Chief

India has weathered crises before by combining policy agility, institutional confidence and citizen resilience. This moment will require all three.

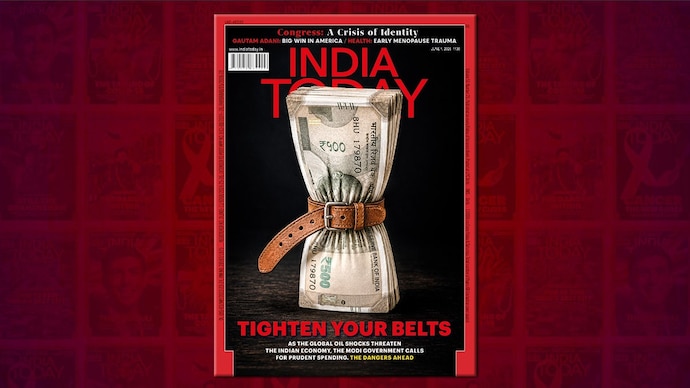

ISSUE DATE: Jun 1, 2026 | UPDATED: May 22, 2026 19:10 IST

Three years ago, India emerged successfully from what could be called its economic long Covid. That spoke of buffers deep enough to absorb unforeseen shocks. We now face another external crisis, and it may prove to be a sterner test of our resilience. The supply choke at the Strait of Hormuz caused by the Iran War has plunged the pricing dynamics of crude oil, fertilisers and an entire suite of essentials into prolonged uncertainty. For India, this hits an Achilles’ heel. We depend substantially on imports of precisely these commodities to guarantee our energy sufficiency as well as food security. Prime Minister Narendra Modi’s May 10 appeal to the nation to practise prudence on certain forms of consumption is, therefore, an advance warning to brace for difficult times ahead. Modi sought thrift from India by working from home wherever possible, cutting foreign travel and destination weddings, not buying gold, reducing edible oil and fertiliser use and buying swadeshi merchandise.

These may sound like random acts of thrift. They are not. They are linked to one central concern: India’s current account deficit (CAD), the gap between foreign currency inflows and outflows, is deteriorating due to runaway prices. Crude basket rates have risen 55.3 per cent since last May for India. Our net oil and gas import bill of $117.5 billion in FY26, 15 per cent of our total import bill of $775 billion, will spike up. Edible oil prices are 12 per cent higher than a year ago. Again, over half of our needs are met by imports, which last year cost $20 billion. Global urea prices have skyrocketed by 60 per cent; so, our fertiliser import bill will also increase beyond the $15 billion spent last year. Together, these two heads threaten to well exceed the 5 per cent they constituted in our FY26 import bill.

Then, there are the more clearly discretionary items. Gold imports had doubled in value last year, costing India $72 billion, nearly 10 per cent of our import bill. Other big-ticket items like foreign travel ($35 billion) and imported consumer goods ($90 billion) constituted an outflow of 18 per cent of our foreign currency reserves. India’s trade deficit, $310 billion in February, is set to widen. Experts expect the CAD, now 1 per cent of the GDP at $30 billion, to rise to 2.3 per cent in FY27.

This is not yet a balance of payments crisis. India’s foreign exchange reserves, at $697 billion in May, are in a theoretically healthy zone—we had averaged $150 billion in the 2000s, $360 billion in the 2010s, and have only edged down from an all-time high of $728.49 billion in February. But headline reserves can flatter. A fifth of that $697 billion is actually gold, which the Reserve Bank of India (RBI) had been stocking up on. The Foreign Currency Assets component, the actual cash in hand, had tumbled 4 per cent to $552.4 billion between February and May as the RBI dipped into the pool to shore up the rupee, which is presently threatening to breach the psychological barrier of Rs 100 to the dollar.

That cushion must be judged against the scale of the outflow. The items marked for austerity accounted for nearly half of our FY26 import bill of $775 billion. They will now become much costlier. Nor is pressure likely to be offset by capital inflows. FDI has been largely negative for six months, and a record $26 billion repatriated out of India since January, leaving Foreign Portfolio Investments at $850 billion. The pressure on the exchequer is also fiscal. The pro-consumer fuel tax cuts of late March cost Rs 500 crore a day; that would have eaten up 12 per cent of India’s capex outlay in FY27. That’s when petrol and diesel prices, unchanged for four years, were finally hiked twice in May. Costlier fertilisers imports, likewise, could jack up the farm subsidy outgo beyond Rs 2 lakh crore in FY27 unless prices are hiked, a politically difficult decision. Whether the government carries the burden, companies or consumers, the pain will radiate through the economy. Experts foresee growth declining by a whole point to 6.5 per cent in FY27.

This week’s cover story hands you a comprehensive map of where we are within the maze, and how we could find a way out. Besides appeals to conscience, the government moved to curb India’s enthusiasm for gold and silver by more than doubling import duties to 15 per cent. There’s talk of reviving the Gold Monetisation Scheme, to get some of the 30,000-odd tonnes lying with Indian households into productive play. In other sectors, there are no good options. Electric vehicles remain a promising alternative, but they are still plagued by range anxiety and barely cover 4 per cent of India’s 400 million registered vehicles. Organic farming is desirable but complex and costly for most farmers. Food is notoriously resistant to behavioural modification, so the picture of conscience-stricken Indians abstaining from fried savouries is too idealistic. Yet modest restraint under all these heads can realistically save about $15 billion. That is worth treating seriously as policy, not just symbolism.

The broader scenario is worrying. We are moving into a stagflationary world. Expect weak exports, falling Gulf remittances and, in Modi’s words, “the return of massive poverty” if the crisis deepens. India has weathered crises before. It has done so by combining policy agility, institutional confidence and citizen resilience. This moment will require all three. The turbulence has begun. The question is not whether it will hurt. It is how well prepared we are to absorb it. In short, time to tighten our belts.

- Ends