The $100 barrel is back. India's rate-cut hopes are the first casualty

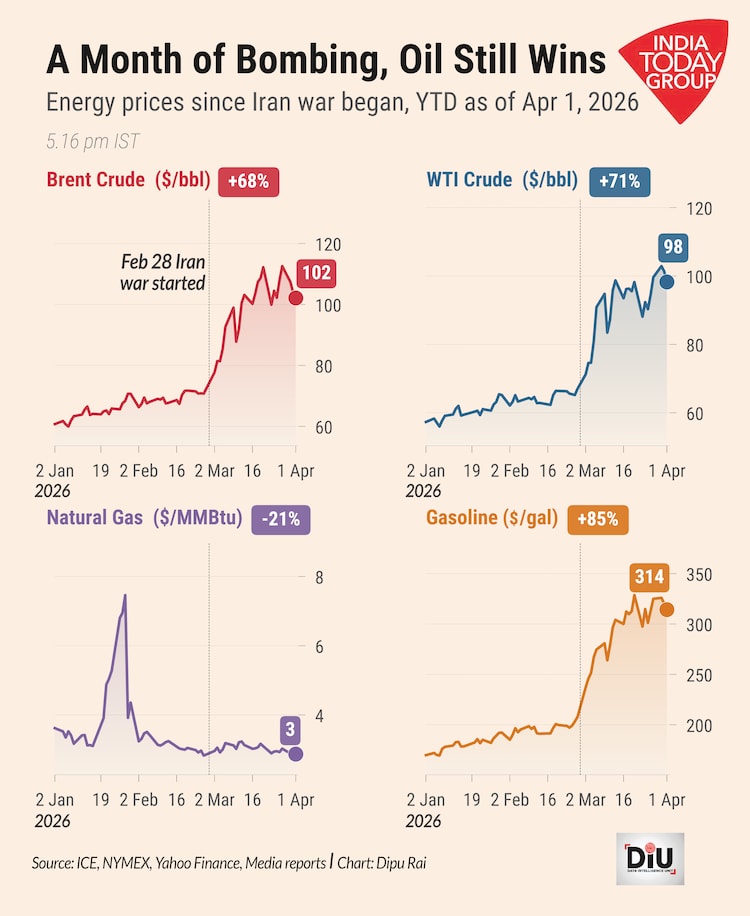

Brent Crude has surged 68 per cent since January as the war in Iran chokes the Strait of Hormuz. The RBI now faces a painful choice between growth and inflation.

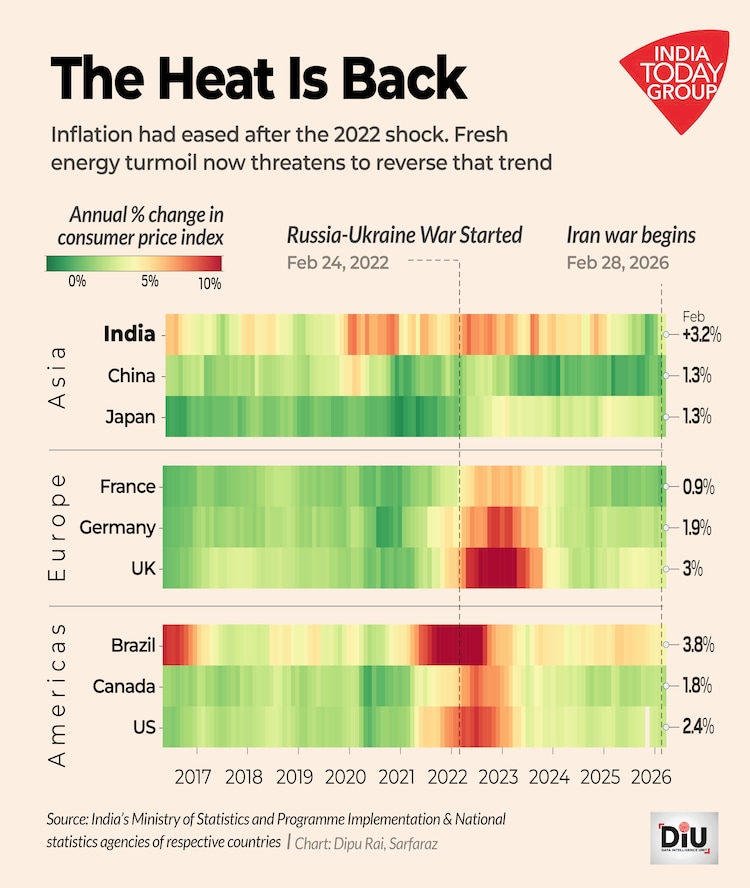

Central bankers thought they had beaten inflation. They were wrong.

After peaking above 10 per cent across the rich world in late 2022, driven by post-pandemic supply-chain breakdowns, excess stimulus, and the energy shock from Russia's invasion of Ukraine, consumer prices had been falling steadily.

By early 2026, average inflation in advanced economies hovered near two per cent. The beast, it seemed, had been tamed.

Then came the bombs.

America's and Israel's war against Iran, which began on February 28, disrupted energy markets with a speed that caught policymakers off guard. Flows of oil through the Strait of Hormuz remain roughly 95 per cent below normal levels.

Outmatched on the battlefield, the Islamic Republic retaliated by bombing natural-gas plants across the Gulf. The result: Brent Crude reached USD 102 a barrel on April 1, up 68 per cent from $60 at the start of the year. American gasoline prices have jumped 85 per cent to USD 3.14 a gallon.

For India, the world's third-largest oil importer, the timing could not be worse.

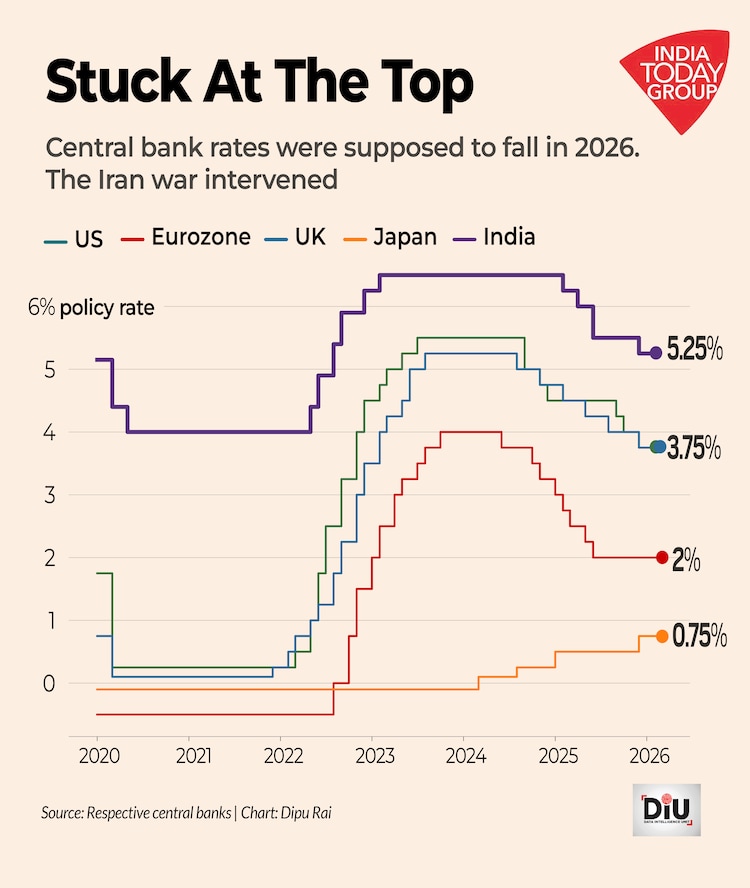

RBI'S RATE-CUT WINDOW JUST SLAMMED SHUT

The Reserve Bank of India had been preparing to ease monetary policy. Inflation was within its four per cent target. Growth needed support. Rate cuts were on the table.

The Iran war changed the arithmetic overnight.

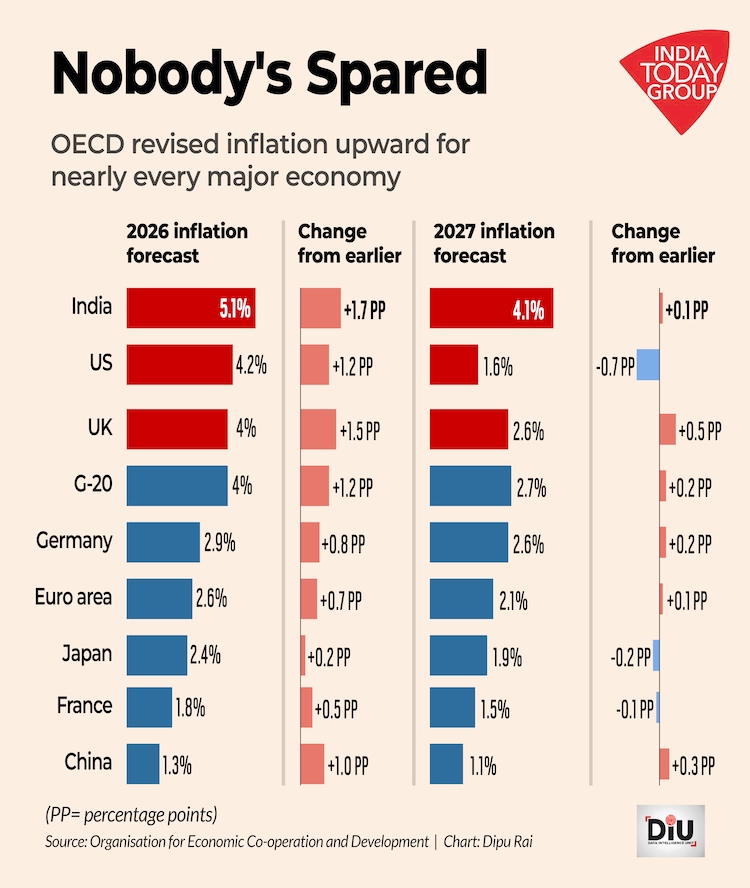

The Organisation for Economic Co-operation and Development revised India's 2026 inflation forecast to 5.1 per cent in March, a jump of 1.7 percentage points from its earlier projection — and the largest upward revision in the G20.

The United States was revised to 4.2 per cent (up 1.2 points), the United Kingdom to four per cent (up 1.5 points). For 2027, the OECD now projects India at 4.1 per cent.

"A USD 10-per-barrel increase in crude oil prices could widen the current account deficit by USD 16.7 billion, increase currency weakness and push inflation," said Devendra Kumar Pant, chief economist at India Ratings and Research. "Average inflation in the base case scenario is now expected to be 4.1 per cent compared to the earlier forecast of 3.7 per cent, and the currency may weaken 4.5–5 per cent year-on-year in FY27."

India Ratings and Research expects the RBI to hold policy rates through FY27.

OIL AT $100: WHAT IT COSTS INDIA

India imports more than 80 per cent of its crude oil. Every dollar added to the price of a barrel ripples through the economy, from diesel at the pump to fertiliser subsidies in the budget.

Since the war began, the government and oil marketing companies have scrambled to absorb the blow:

- LPG prices: Up Rs 60 per cylinder (14.2 kg)

- Premium petrol: Up Rs 2 per litre

- Industrial diesel: Up 25 per cent

- Excise duty: Cut by Rs 10 per litre on petrol and diesel

- Export duties: Increased on petrol and diesel

The excise duty cut alone, if maintained through FY27, will cost the government an estimated Rs 1.70 lakh crore, according to India Ratings and Research.

At current international prices, oil marketing companies absorb under-recoveries of roughly Rs 26 per litre on petrol and Rs 81.9 per litre on diesel, an estimated Rs 2,400 crore per day.

The diesel crack spread — the gap between refined diesel prices and crude — more than doubled between November 2025 (USD 26 per barrel) and March 2026 (USD 52 per barrel). The reason: Middle Eastern refinery exports skew toward diesel and middle distillates, making diesel markets more exposed to the loss of Gulf refining capacity. Petrol spreads, by contrast, fell to USD 7.4 per barrel from USD 14.4 over the same period, because petrol demand is more seasonal and discretionary.

India Ratings and Research modelled four inflation paths for FY27, assuming crude averages USD 110 a barrel in the first quarter, declining to USD 80 by the fourth. "If the higher prices and supply shortages continue for a long time, the government may follow a pricing policy similar to our base case or scenario 3, and inflation in FY27 may average in the 4.0 to 4.5 per cent range," it noted.

GLOBAL PICTURE NO BETTER

President Donald Trump said on Tuesday that the United States could withdraw from Iran "whether we have a deal or not," signalling growing impatience with a war that has sent energy prices spiralling. With gasoline hitting USD 4 a gallon in the US, inflation is back on America's radar.

But the sharpest revision belongs to Britain. The OECD now projects UK inflation at four per cent for 2026, up from 2.5 per cent, the highest in the G7 after the US. Across the G20, the 2026 inflation forecast rose 1.2 percentage points to four per cent.

The post-pandemic disinflation that central bankers celebrated is unwinding in real time.

WHAT TO WATCH

Three variables will determine how deep these cuts.

Duration of the conflict: A quick resolution, which Trump's comments hint at but do not guarantee, would allow oil prices to retreat. A prolonged war keeps prices elevated and amplifies second-round effects through freight costs, supply shortages and reduced economic activity.

Speed of supply restoration: Even after hostilities end, bombed-out gas plants and disrupted shipping routes take months to restore. The longer the disruption, the wider the damage.

Pass-through decisions: The Indian government has historically shared the burden of oil shocks among consumers, oil companies and the exchequer. How much pain reaches consumers will determine whether inflation stays near four per cent or pushes toward five per cent.

India's continued dependence on energy imports remains, as India Ratings and Research puts it, “a key macro weakness.” The war has exposed that weakness in full. The inflationary beast, it turns out, was only sleeping.